Job losses and investment cuts: Study finds increasing EU rPET imports, causing “alarming” industry effects

27 Feb 2024 --- PET recycling imports to the EU from non-OECD countries are rising, risking the slowing down of investments and jobs throughout Europe’s PET value chain, according to a new study report.

The report was commissioned by chemical recycler Eastman and financed by Eastman and plastic recycling and packaging company Interzero.

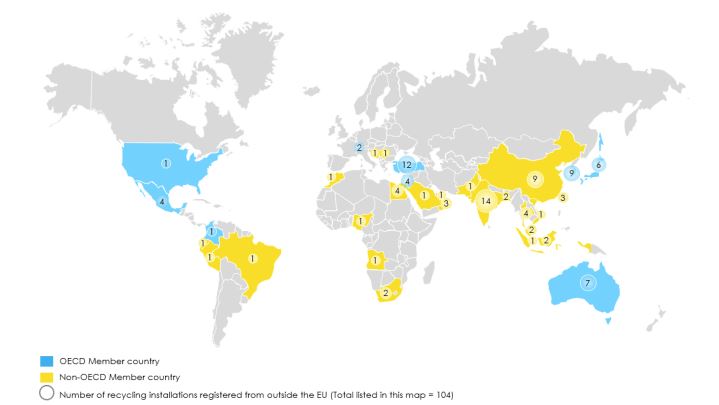

Significant PET recycling capacity outside the EU is permitted for import of contact-sensitive recycled PET (rPET) into the EU. Last October, the EU’s Directorate-General for Health and Food Safety announced that approximately 100 recycling or decontamination installations outside the EU (not including the UK) are accredited for import of recycled plastic materials and articles intended to come into food contact.

Over half of these registrations are in non-OECD countries, where the export of plastic waste from the EU will be prohibited. This means that in the future, any rPET imported from non-OECD countries would not be from EU PET waste, meaning the EU would use other countries’ waste to meet its targets, warns the report.

Ton Emans, president at Plastics Recyclers Europe, tells Packaging Insights that EU imports of bottle-grade recycled material come from various non-EU countries, mainly located in Asia. “The highest number of imports comes from China, Vietnam, Türkiye and Egypt,” he says.

Approximately 100 installations outside of Europe registered to sell recycled plastic approved for use within the EU (Image credit: Eastman and Interzero).Stalling EU investments

Approximately 100 installations outside of Europe registered to sell recycled plastic approved for use within the EU (Image credit: Eastman and Interzero).Stalling EU investments

Delivery of the Ambitious Complementarity Scenario (ACS) by 2040 requires European collection, sorting and recycling infrastructure capacity to almost triple from 2020 to 2040. In this scenario, mechanical recycling capacity would expand from 2–3.3 metric tons annually by 2040, while chemical PET recycling would grow from negligible capacity today to 2.1 tons annually by 2040.

Building this scale of recycling infrastructure is estimated to require €17 billion (US$18.5 billion) in investment in sortation facilities and mechanical and chemical PET recycling.

But Eastman and Interzero stress that increasing capacity for imports of recycled PET into Europe could negatively impact investor confidence and slow or stall future investments in new collection, sorting and recycling infrastructure in Europe. The recycling industry in Europe has raised the alarm about this potential effect.

PPWR to avoid “deindustrialization”?

Emans says that the current policy direction taken in the PPWR trilogues would allow using imported recycled content to meet recycling targets which would have “dramatic” consequences for the EU’s industry.

Ton Emans, president at Plastics Recyclers Europe.“That is why a regional circularity perspective is so important, and the so-called proximity principle — in line with the environmental objectives of the EU, where waste is managed as near as possible to its place of production.”

Ton Emans, president at Plastics Recyclers Europe.“That is why a regional circularity perspective is so important, and the so-called proximity principle — in line with the environmental objectives of the EU, where waste is managed as near as possible to its place of production.”

“Furthermore, this measure must be supplemented by verification measures, applicable also to imports (based on third-party certification) paired with establishing conditions that are equivalent to the requirements of the relevant Union environmental law (equally applicable to imported recycled materials), without which Europe’s efforts to transition to a circular economy would be seriously undermined,” asserts Emans.

“Ensuring a level playing field for EU and non-EU plastic waste and recyclates in the PPWR is essential, particularly in a geopolitical context where non-EU actors are not playing by the same rules. If measures are not implemented urgently, the EU will suffer further deindustrialization.”

Threatening EU jobs

Two new system scenarios illustrate the potential implications for Europe if rPET imports were to stall or slow future investments in the scale-up of European recycling systems:

Scenario A: Investment in new sorting and recycling infrastructure in Europe stalls between now and 2040 due to high levels of imports. This scenario assumes that no additional sorting and recycling infrastructure is built, resulting in an average recycling rate of PET/polyester in 2040 of 32% (vs. 67% in the ACS).

This scenario would generate 5.2 metric tons of non-recycled waste annually (vs. 2.5 metric tons annually) and 8.2 metric tons of CO2 emissions annually of end-of-life GHG emissions in the EU (vs. 3.7 metric tons of CO2 emissions annually).

Scenario B: Investment in new sorting and recycling infrastructure in Europe slows compared to the ACS scenario. This scenario assumes that legislative changes are enacted for effective Deposit Return Systems for PET beverage bottles across Europe (with associated sorting and recycling infrastructure scaling up in Europe), but no additional sorting and recycling infrastructure for other PET/polyester is built.

In this case, the average recycling rate of PET/polyester in 2040 would be 38%, with 4.7 metric tons annually of non-recycled waste and 7.4 metric tons of CO2 emissions annually of end-of-life GHG emissions in the EU.

If investment in European PET recycling and reuse infrastructure decreases, job creation opportunities in collection, sortation and reuse or recycling will be affected, warns the study. Relative to the ACS (estimated 28,000 net new jobs in 2040), scenarios A and B are estimated to create 10–11,000 fewer overall jobs in the PET value chain in Europe in 2040.

By Natalie Schwertheim